Banking in open ecosystems

July 21, 2019 • ☕️ 6 min read

More than twenty years ago, Bill Gates famously concluded that “we need banking, but we don’t need banks anymore”. He was taking a gibe at how slowly banks were responding to technology disruption and how strongly they were clinging to the traditional model of banking. I think he was wrong about his conclusion. In fact, we can see that banks have flourished over recent decades without needing to change very much. But I also think that the potential of technology has not played itself out and I would like to offer a different vision of what digital technology can mean for banks.

As much as Fintechs have offered interesting digital services in every part of financial services (payments, investing, trading, lending, advising, etc), banks still play a unique role in the economy. They carry the weight of trust of regulators (and implicitly society) to manage clients’ risk. Managing risk means such things as protecting clients’ assets, lending responsibly, and managing mismatches between assets and liabilities. While fintechs can cover some niches, there has been little change when it comes to large scale aggregation and management of risk, which is the very heart of banking. In essence, most fintechs are still appendages to the traditional banking system, rather than offering an alternative banking model. Fintechs often use banks’ services (leading to the drive towards open banking).

The real disruption will come from banks discovering how to be better banks, which really means how to manage risk better at the core of their business, rather than merely appending digital services to this core.

Risk management is largely about information - the more information we have about the world, the better we can navigate its risks1. On the face of it, this would seem to give the technology giants a route into banking, because they are masters at gathering and analysing information. But, in practice, banks have much greater information about what really matters to them. Banks understand their clients’ intimate financial affairs, not just their “social” activity (social activity is a much less direct way of understanding financial risk). Banks also aggregate client information relatively efficiently with data from financial markets and the economy.

For this privilege banks are heavily regulated, which protects them more than it holds them back.

What would be game changing for commercial banks?

When considering the privilege that banks already have, what game changing client information would help them manage risk better (and therefore, offer cheaper financial services, experience fewer losses and scale better)?

I think one answer to this is that banks would love to have more information about their clients’ clients and their clients’ suppliers, and their mutual transactions — or more generally, to understand the ecosystem (or business community) in which their clients operate, because risk changes significantly when understood in the context of the entire ecosystem — if banks understand who trades with whom, and the obligations they have to each other, the risks can be more efficiently managed.

The thing is that clients are not going to give banks this information. In the age of Facebook and Google, and the broad reactions against the excesses of data exploitation, businesses will be more vigilant than ever about sharing information, even if banks coax them by offering free services (as Google does). The last thing that clients want is for their banks to emulate Facebook.

IOUze

At IOUze we are helping banks and fintechs to explore solutions to managing risk in an ecosystem. This helps them to offer enhanced financial services at lower risk. We believe that this is the future of transactional banking.

We believe that there is a different form of “open banking” that is more than just technical APIs, that allows businesses, consumers and banks to connect business processes in a semi-decentralised model2. It needs to be somewhat decentralised, because it is not possible for banks to completely control their ecosystems. Essentially, some central control is given up to connect more directly with clients.

IOUze achieves this by essentially creating a network of financial agreements that are grounded in the day-to-day operations of business communities. It is an open, extensible internet of financial data.

The net effect is that banks connect into the ERP processes of clients (which they have done previously with some of their largest clients at great cost and effort). But most importantly it also allows them to connect (in a controlled way) with the clients’ clients and the clients’ suppliers. On top of this capability, the bank can create much richer services for their clients at lower risk and much improved user experience.

Example use case

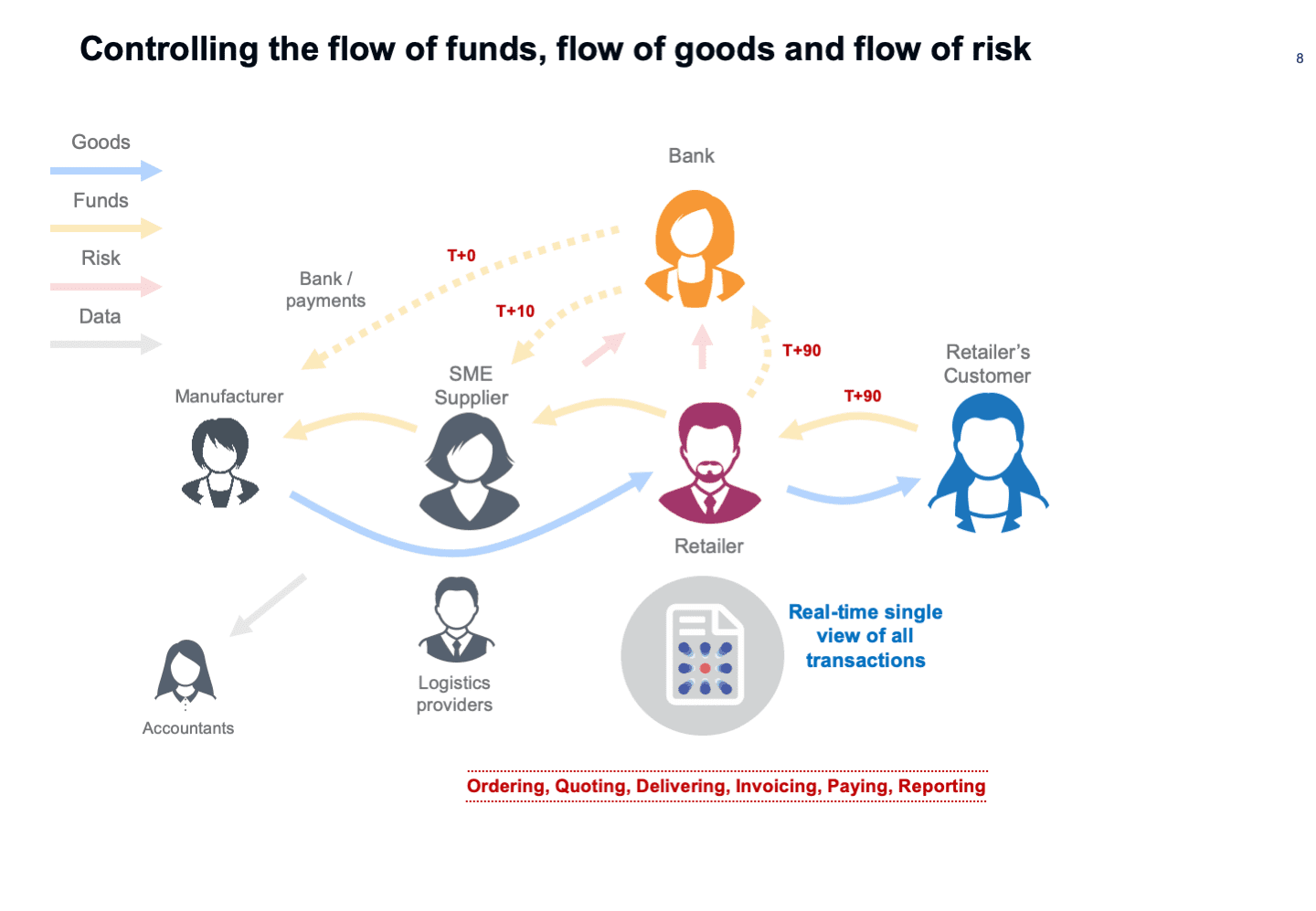

IOUze is a network of verified financial transactions, shared in a business community with very little effort.

For example, a small supplier receives a purchase order from a large retailer on the IOUze network. The supplier accepts the purchase order, and this updates in real-time on the buyer’s ERP system. Later, the supplier delivers the goods, which are accepted by the buyer. The supplier issues an invoice with the agreed terms of payment (90 days). The invoice is authorised automatically or by a manager in the retailer. All of these operations are verified in real-time on the IOUze network.

Using IOUze secure access controls, the retailer reveals the supplier’s banking details, payment terms and the total invoice amount to their bank, which will execute the payment on the due date.

The approved invoice and signed delivery note recorded on IOUze are used to prove that the supplier has met their obligation and that the risk of payment is now mostly on the large (well trusted) retailer. This allows the bank to provide affordable supply chain financing to the supplier at low risk, and with almost no administrative overhead.

The ecosystem can be expanded to the manufacturer and the consumer to create a true end-to-end digital experience that reduces costs and risk. It can also include other service providers, like logistics providers, accountants, regulators, etc. All participants receive accurate, verified, real-time data for almost no effort.

How this works

This network of trusted financial agreements is possible because we have used cryptography to design unique features into the IOUze network:

-

Data is Self Sovereign which means that it is controlled by the subject of the data, who can share it in a highly secure way with other participants in their business community to facilitate real-time, low-cost and low-risk transactions. “Just enough” of the data can be shared to allow processes to work. There is no central organisation that has access to the data.

-

Data is verified, which means that one can prove (using cryptography) who issued the data, and once issued it is impossible to change or delete (without the change being obvious to the network). Other participants can sign the data to make specific claims about events in a business process. These signatures are equally verifiable.

-

Data can be used to prove performance of the participating businesses (using advanced cryptography known as zero knowledge proofs). A performance metric can be published and proved without revealing the underlying data. These metrics could be credit scores, turnover, etc.

Transactional banking technology

The IOUze network offers opportunities for a new generation of transactional banking platforms that connect business communities and their day-to-day processes. It allows a bank to integrate business services and financial services. At its heart, it measures and transfers risk more efficiently. This allows banks to lead the emergence of more digital banking models.

Notes

[1] Actually risk management also relies on models to process information, but I think the models are less differentiating than information, especially as regulators try to standardise risk management methodologies.

[2] Decentralised business models refer to blockchain-type platforms with no central authority (like Bitcoin). IOUze is decentralised, but has a necessary level of governance and controls, which we don’t outline in detail in this post.

Photo credit

Photo by Marvin Meyer on Unsplash